Legal context

Insolvency Law

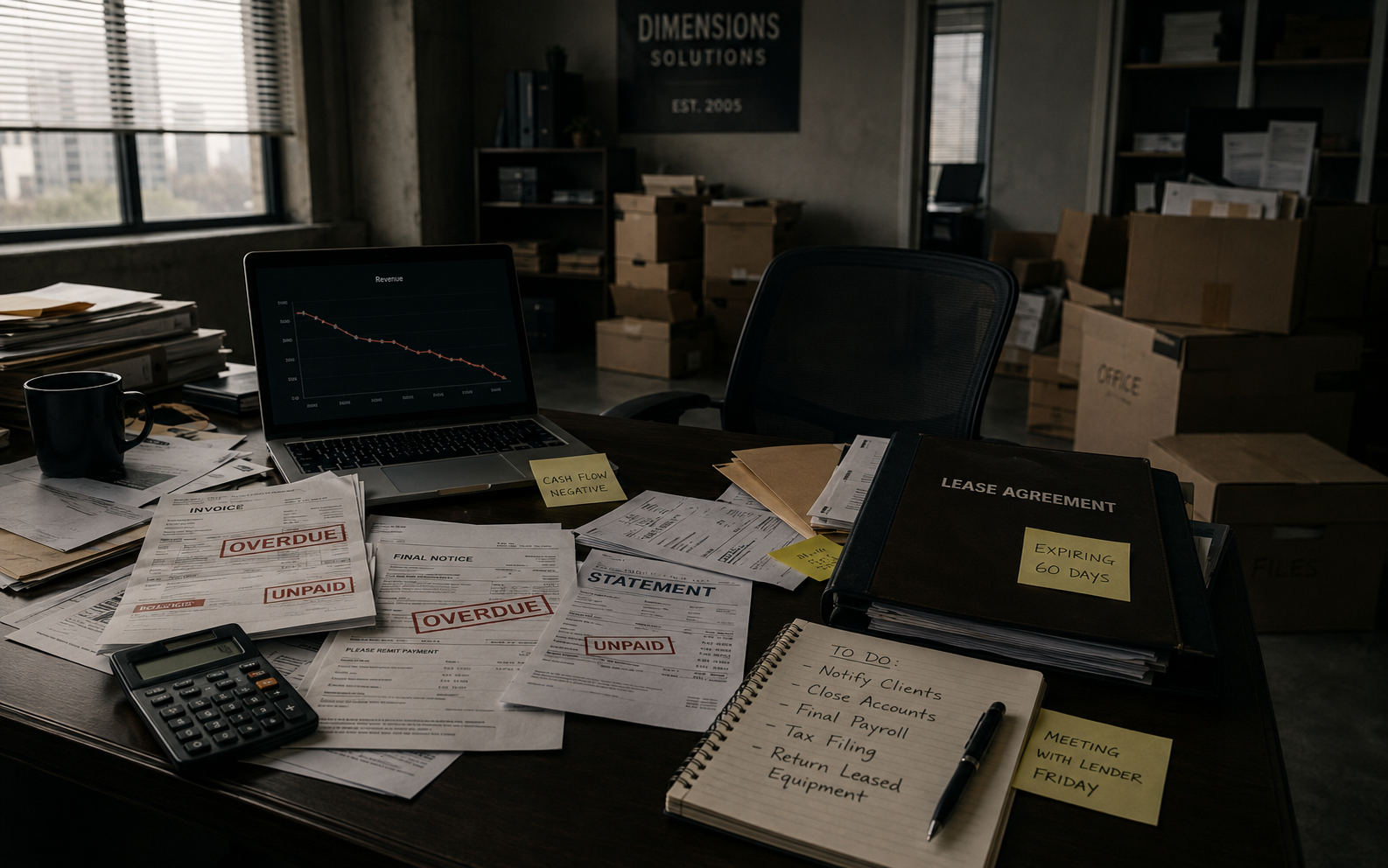

Insolvency law deals with financial distress before, during and after formal sequestration, liquidation, business rescue or compromise processes. It includes debtor advice, creditor remedies, asset protection, suretyship exposure and claims against insolvent estates. The correct procedure is often as important as the merits of the matter. A missed notice, incorrect court process or poorly drafted document can affect the client's legal position, costs and available remedies.

The main legal framework includes the Insolvency Act 24 of 1936, the Companies Act 71 of 2008, business rescue provisions in Chapter 6 of the Companies Act, the Master's supervision of trustees and liquidators, and court procedure in the High Court and Magistrates' Courts where relevant. Depending on the issue, the matter may involve the High Court, CIPC, the Master of the High Court or creditor negotiations. The correct route must be selected at the start because insolvency procedure, notices and evidence requirements differ.

Clients usually need an attorney when income has reduced, creditors are threatening legal action, a business is in distress, assets have been attached, a debtor wants to restructure payments, or a creditor suspects that assets are being moved out of reach. Early legal input helps identify the client's rights, the correct process, the evidence needed and whether negotiation, mediation, urgent relief or formal proceedings are appropriate.